It’s Nvidia’s World: How Advisors See the Next Phase of AI

Nvidia remains the undisputed center of gravity for the technology sector, but financial advisors and asset managers are quietly shifting their playbooks for the next phase of artificial intelligence. While the initial wave of the AI boom was defined by a frantic race to accumulate raw hardware, the current environment demands a much more nuanced approach to portfolio construction. Leading wealth management firms are looking past immediate earnings volatility, focusing instead on how the chip giant is leveraging its massive balance sheet to entrench itself as the permanent architect of the global AI ecosystem.

Rather than treating the company as a cyclical semiconductor manufacturer, market analysts view its unparalleled market position as an infrastructure play that extends well into the next decade. For instance, data tracked by the ETF Database highlights massive inflows into concentrated semiconductor and generative AI exchange-traded funds, signaling that advisors are still aggressively using the company as their primary vehicle for tech exposure. However, the strategic conversations taking place behind closed doors are no longer just about quarterly unit shipments of Blackwell or Rubin architecture chips; they are about ecosystem dependency, capital allocation, and software moat sustainability.

Moving from Shovel Seller to Ecosystem Architect

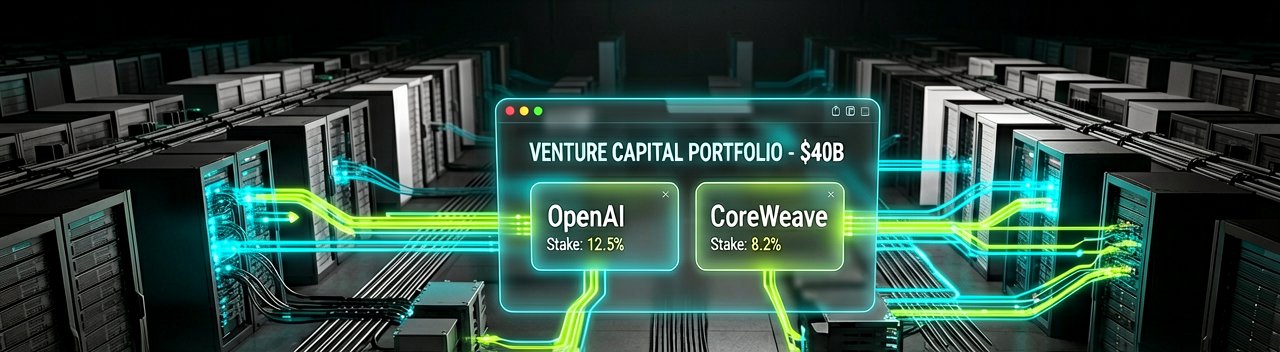

What Most Reports Miss: The narrative surrounding the hardware leader often focuses strictly on demand from hyperscale cloud providers, but seasoned investment advisors are paying closer attention to the company's aggressive venture strategy. In early 2026, the tech giant topped an astonishing $40 billion in equity bets, effectively recycling its massive free cash flow back into the very companies that buy its hardware. According to a detailed breakdown by TradingView , this multi-billion-dollar investment web includes massive commitments like a $30 billion stake in OpenAI, alongside multi-billion-dollar allocations to data center operator IREN, Corning, CoreWeave, and Nebius Group. By funding foundational model creators and critical infrastructure providers simultaneously, the company is systematically ensuring that the next wave of data centers will be built entirely around its proprietary technology stack.

This circular investment model has ignited a fierce debate among Wall Street analysts and wealth managers regarding the true nature of organic market demand. Bullish advisors view these capital deployments as a brilliant competitive strategy that secures hardware allocations, builds long-term customer lock-in via the proprietary CUDA software ecosystem, and establishes a diversified foothold across the entire AI value chain. Skeptics, conversely, wonder whether these multi-billion-dollar equity injections are artificially propping up hardware sales, raising valid questions about how much of the broader AI demand is entirely organic versus supported by the manufacturer's own financing operations.

Meanwhile, portfolio managers are looking at the long-term duration of this buildout to calm jittery clients facing market volatility. Analysts from firms like Financial Post note that robust multi-year guidance provides clear reassurance that the massive capital expenditure boom is not a short-term trend, but an infrastructure cycle stretching comfortably into 2027 and 2028. As enterprise adoption matures, advisors are increasingly advising clients to focus less on short-term price fluctuations and more on the institutional transformation occurring as corporations integrate agentic AI applications directly into their bottom-line operations.

The Fine Print of the AI Supercycle

Reading Between the Lines: The prevailing Wall Street consensus operates on the comforting assumption that capital expenditure from the world’s largest cloud providers can grow at triple-digit rates indefinitely. Yet, a sober look at the macroeconomic math reveals a widening disconnect between the trillions of dollars pouring into physical data center infrastructure and the actual revenues generated by enterprise AI software. Wealth managers are increasingly forced to balance the euphoria of flawless quarterly earnings reports against the stark reality that many corporate clients are still struggling to find a clear path to monetization for their expensive generative AI pilots.

This massive gap between infrastructure supply and consumer-facing demand introduces a layer of structural risk that many retail investors are completely overlooking. If hyperscalers begin to experience a deceleration in their own cloud revenue growth, their ability to fund massive, continuous hardware refreshes every eighteen months will inevitably face intense scrutiny from institutional shareholders. For advisors, the strategic challenge is no longer about picking the winner of the hardware race, but about timing the precise moment when the market shifts its focus from theoretical compute capacity to tangible corporate productivity gains.

Furthermore, the chipmaker's strategy of investing directly in its own customers creates a complex financial loop that could amplify market corrections if the AI startup ecosystem faces a funding crunch. While these equity investments lock in near-term hardware orders, they also bind the semiconductor giant's valuation directly to the speculative stability of pre-revenue AI developers. Should the venture capital market cool down, the sudden devaluation of these tech assets could send shockwaves through the broader market, transforming what looked like a brilliant ecosystem moat into a highly concentrated risk vector for global portfolios.

"Investing in the current AI landscape is like buying a ticket to a high-stakes poker game where the dealer also happens to own the casino, the hotel, and the company that prints the cards—you might win a few hands, but you should probably keep one eye firmly on the exit doors."

Artūras Malašauskas is an AI Systems Integrator with 20+ years of production-grade web engineering experience. He has designed, shipped, and scaled enterprise Python/PHP systems for logistics, SaaS, and public-sector clients. For the past year, he has focused exclusively on AI integrations: deploying open-source LLMs, building generative media pipelines (image, audio, video), and engineering multi-agent workflows for real production environments. His standard: reproducibility, security, cost-efficient inference—no vaporware. He documents and evaluates emerging AI tooling, separating verified capabilities from marketing noise. Technical editor at: muza-ai.eu, ai-verslas.lt, ai-naujinos.lt Connect on LinkedIn

Comments