The Psychology of Past-Due Accounts: How SymendConverse Weaponizes Behavioral Science for Automated Collections

The debt recovery sector is undergoing a massive shift from aggressive tactics to automated, empathetic outreach. Traditional collections processes frequently struggle to engage financially stressed borrowers, which leaves valuable capital unrecovered and damages long-term customer relationships. To bridge this gap, tech enterprise Symend launched a new tool called SymendConverse to combine advanced generative AI with deep psychological insights. According to an official press release published by Newswire, this voice-enabled conversational agent interacts with delinquent customers using behavioral science strategies rather than rigid, automated scripts.

The roll-out of SymendConverse marks a clear evolution in enterprise risk management. Prior software automation focused almost entirely on optimization and high-volume digital outreach, which frequently resulted in consumer avoidance and digital fatigue. By introducing conversational AI tailored to distinct delinquency archetypes, Symend expands its core product ecosystem alongside SymendCure and SymendPrevent, per the tracking report from Yahoo Finance . This multi-layered strategy aims to maximize account normalization across major utility, automotive financing, telecom, and banking operations.

The Strategy of Archetype Personalization and Real-Time Negotiation

Unlike generic conversational AI agents that rely on horizontal language models, SymendConverse applies behavioral dynamics directly during live voice interactions. The software evaluates the customer's financial capacity and emotional state to classify them into behavioral profiles. This immediate assessment informs the agent's tone, dialect choices, and negotiation logic. During a call, the system adapts dynamically to offer tailored installment plans or deadline extensions based on structural boundaries rather than strict binary requirements. If a consumer presents an unusually complex financial issue, the tool seamlessly routes the interaction to a live customer support representative, preserving the full conversational context and behavioral history.

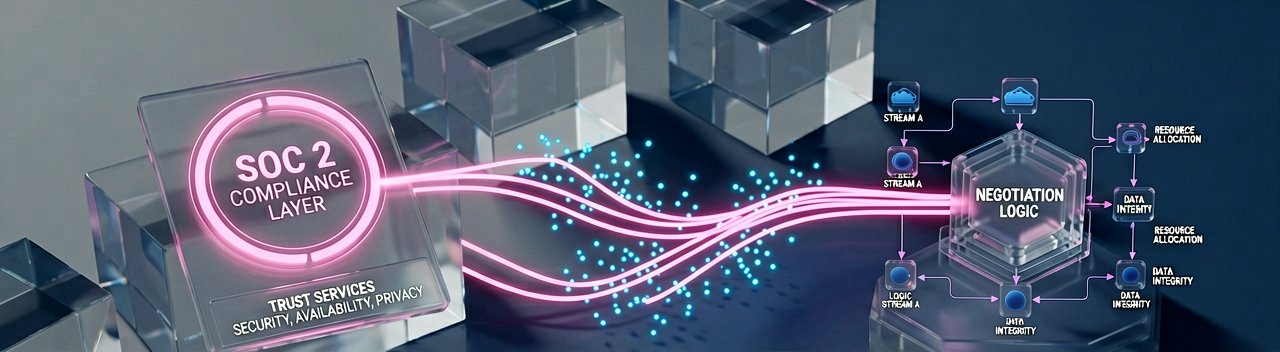

Enterprise Infrastructure Compatibility and Regulatory Alignment

A major technical hurdle for large organizations deploying generative automation is complex, expensive system restructuring. Symend avoids this bottleneck by engineering SymendConverse to serve as an orchestration overlay that integrates with pre-existing contact center systems and telecom frameworks. According to product design details shared on MarTech Cube , organizations can maintain their established voice technologies while letting Symend control the psychological strategy, data analysis, and outreach orchestration. This modular structure allows companies to swap or upgrade their foundational speech synthesis engines without changing their overall platform. Furthermore, the architecture complies with strict data handling frameworks, including SOC 2 Type II, ISO 27001, GDPR, and PCI DSS standards.

The Financial Context: Moving Beyond Basic Automation Gains

The enterprise adoption of behavioral AI highlights a major limitation in traditional financial software. Simple automation often produces a brief spike in customer engagement that quickly plateaus once the volume of outbound outreach peaks. As noted in a market review by AInora, data platforms deliver superior returns when they shift from merely predicting high-risk accounts to actively understanding the underlying psychological barriers that stop a consumer from paying. Symend states that its unified behavioral ecosystem has resolved more than 250 million delinquencies and recovered over $50 billion across its target industries. As financial institutions deal with fluctuating consumer credit health, the integration of real-time behavioral insights into automated workflows is transforming from an experimental feature into a standard requirement for preserving customer lifetime value.

Behind the Scenes: Inside the Behavioral Engineering of Modern Risk Platforms

The technical engineering driving SymendConverse goes far beyond standard speech-to-text algorithms or template-driven chat frameworks. For decades, the financial services sector relied on crude credit-scoring metrics and static outreach schedules to manage delinquent accounts. If a borrower fell into arrears, automated dialing systems would systematically trigger high-volume phone campaigns at standard legal intervals. This traditional approach prioritized volume over engagement, treating every late payer as a uniform compliance liability rather than an individual navigating unique financial obstacles. Behind the scenes, the current shift toward behavioral AI changes this model by prioritizing real-time cognitive evaluation over simple collection volume.

Product developers and behavioral scientists working on these systems start by mapping specific consumer emotional profiles. When a customer falls into delinquency, their cognitive processing is frequently compromised by acute financial stress, which triggers defense mechanisms like avoidance, denial, or hostility. Experienced collectors know that a confrontational tone almost always causes the consumer to hang up or ignore future communications. SymendConverse replicates this professional human instinct digitally by using behavioral triggers that minimize friction. The platform uses natural language processing to detect anxiety or frustration in the borrower's voice, immediately adjusting its language to reduce defensive reactions and build cooperation instead.

This nuanced psychological engineering is especially vital for the legal and compliance teams overseeing retail banking operations. In an era marked by strict consumer protection regulations and intense public scrutiny over automated customer service, financial institutions cannot afford rogue AI hallucinations or aggressive negotiation tactics during a call. Because the platform operates as an orchestration overlay, it keeps conversational responses strictly bounded by preset corporate policies and regulatory limits. Stakeholder reviews indicate that this guardrail system gives risk managers the confidence to deploy automated voice negotiation at scale, knowing the software will never deviate from approved compliance scripts or misrepresent payment terms.

From an operational standpoint, this behavioral shift changes how enterprise call centers manage their human workforce. Instead of spending hours managing low-tier, repetitive collections calls that often lead to employee burnout, human agents can focus on complex, high-risk cases that require genuine human problem-solving. When the AI hands off a call, the live agent receives a detailed summary of the customer's behavioral history, emotional state, and previous payment offers. This detailed transition turns what used to be a frustrating, cold-call transfer into a collaborative financial consulting session, which ultimately protects customer loyalty and improves long-term recovery rates across the entire portfolio.

Reading Between the Lines: The Friction Between Algorithmic Empathy and Fiscal Reality

The enterprise rush to deploy "empathetic" collections software introduces a paradox at the center of modern automated finance. Debt recovery is fundamentally a zero-sum exercise focused on extracting liquid capital from accounts facing acute cash flow constraints. While using behavioral science to reduce borrower anxiety sounds highly ethical, it also functions as a sophisticated conversion optimization tool. The underlying tension lies in the corporate objective: the primary metric for success remains the recovery rate, not the consumer's long-term financial health. Labeling automated collection systems as mental health interventions risks masking a highly efficient extraction mechanism under the guise of corporate altruism.

This dynamic creates a complex challenge for the neural networks running these systems. If an AI platform becomes too persuasive by perfectly mapping a borrower's psychological vulnerabilities, it may inadvertently convince a stressed consumer to prioritize a specific utility bill or credit card payment over essential living costs like food or healthcare. Financial institutions must consider whether an algorithm that successfully bypasses human defense mechanisms might cross the line from helpful guidance into psychological manipulation. As consumer protection agencies turn their focus toward deceptive digital architecture, software that customizes its tone to bypass personal boundaries will likely face intense regulatory scrutiny.

Furthermore, the operational promise of a seamless handoff between AI systems and human teams often minimizes the messy reality of legacy bank infrastructure. Large financial enterprises usually operate on fragmented, decades-old core banking platforms that struggle with real-time data sharing. While an advanced overlay like SymendConverse can analyze emotional nuances on the fly, the institutional systems processing the actual payments often take days to update. If a customer negotiates a flexible, AI-approved payment structure only to receive an automated legal penalty notice the following morning due to a system delay, the fragile trust established by the behavioral algorithm is instantly destroyed.

Over the long term, widespread adoption of these systems may trigger a shift in consumer behavior that diminishes their overall effectiveness. Just as internet users developed "banner blindness" to ignore digital advertising, borrowers will eventually learn to spot the polite, calculated patterns of behavioral AI. Once consumers realize that an automated voice's supportive tone is a standardized software path designed to secure a commitment, the psychological comfort vanishes. When the public learns that acting anxious or using specific phrases triggers a softer negotiation script or an automatic human transfer, the collection process will simply become an optimization game played by both sides.

"We have finally achieved the ultimate milestone in fintech engineering: building a machine that can listen to your financial problems, sigh sympathetically in high-definition audio, and still politely take your last twenty dollars before the live agent even picks up the phone."

Artūras Malašauskas is an AI Systems Integrator with 20+ years of production-grade web engineering experience. He has designed, shipped, and scaled enterprise Python/PHP systems for logistics, SaaS, and public-sector clients. For the past year, he has focused exclusively on AI integrations: deploying open-source LLMs, building generative media pipelines (image, audio, video), and engineering multi-agent workflows for real production environments. His standard: reproducibility, security, cost-efficient inference—no vaporware. He documents and evaluates emerging AI tooling, separating verified capabilities from marketing noise. Technical editor at: muza-ai.eu, ai-verslas.lt, ai-naujinos.lt Connect on LinkedIn

Comments