AI Takes on the Afterlife: Legacy Keeper Drops Automated Estate Platform for Wealth Managers

The traditionally slow-moving wealth management sector just got a major technological jolt. Victoria, British Columbia-based startup Legacy Keeper officially launched its highly anticipated, AI-driven estate planning platform on June 15, 2026, aimed at fundamentally changing how financial advisors handle the Great Wealth Transfer. Founder Alex Mason revealed that the software leverages specialized AI agents to process complex, fragmented files into clean, actionable distribution trees in mere seconds, effectively digitizing a workflow that has long been trapped in heavy paper folders and siloed spreadsheets, as reported by BetaKit .

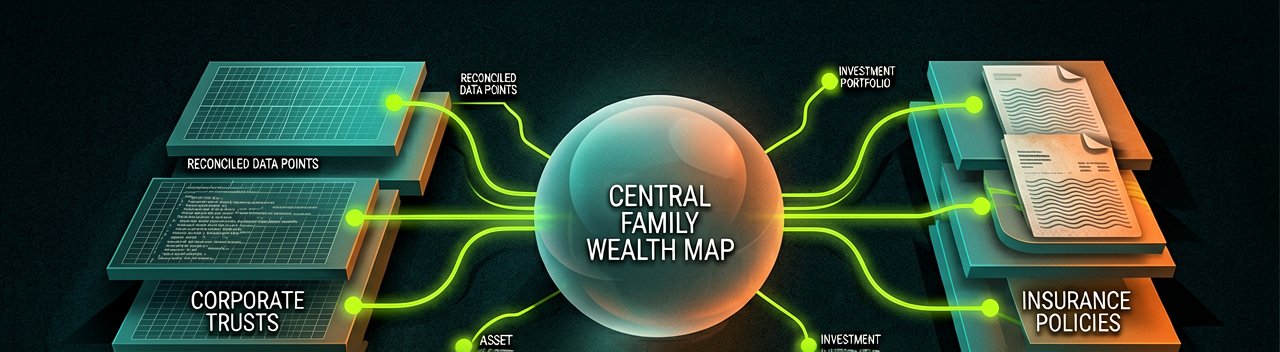

Instead of acting as a basic document storage dump, the platform functions as an interactive ecosystem where advisors can instantly visualize client holdings across insurance policies, trusts, corporate assets, and residual properties. By automating deep data extraction and reconciliation, the software reduces administrative busywork by up to 50 percent. This rapid processing allows wealth managers to spot outdated beneficiary designations or compliance gaps before they trigger costly probate or tax penalties. It is a critical play for an industry scrambling to maintain client retention across generations, especially given that a staggering majority of heirs abandon their parents' financial advisors shortly after inheriting wealth.

Automating the Hard Conversations

The platform introduces a highly context-aware approach to tax regulations, which is a massive selling point for professionals navigating tricky local laws. For instance, in the Canadian market, the system is explicitly built to account for the universal "deemed disposition" rule, which treats an individual's assets as sold at fair market value upon their death. By running localized tax and probate exposure simulations through these specialized Legacy Keeper AI agents, financial professionals can model different asset ownership transfers in real time, turning what used to be a rigid, one-time legal transaction into an ongoing collaborative strategy.

While skeptics often worry that deploying large language models into heavily regulated financial spaces introduces hallucination risks, the fintech space is clearly moving toward these expert-guided systems to lower operational costs. Tech tools do not completely replace the human trust required during emotionally heavy end-of-life planning, but they dramatically lower the barrier to entry for everyday clients. Ultimately, by shifting the heavy lifting of compliance checks and document organization over to AI agents, advisors can finally step away from the paperwork and focus entirely on guiding families through the incredibly sensitive conversations that legacy planning demands.

The Hidden Bottleneck in the Great Wealth Transfer

Beyond the marketing buzzwords: The real crisis driving the adoption of platforms like Legacy Keeper isn't a lack of financial products, but an impending structural collapse in client retention. Wealth management firms are currently facing a massive demographic cliff as trillions of dollars shift between generations over the next decade. Historical data paints a brutal picture for traditional firms: upward of 80 percent of heirs promptly fire their parents’ financial advisors upon inheriting the family estate. This mass exodus happens primarily because the incoming generation views these legacy advisors as outdated gatekeepers wrapped in red tape rather than modern financial partners.

By automating the friction-heavy discovery phase of estate planning, AI agents are attempting to salvage these multi-generational relationships before the primary asset holders pass away. Traditional estate onboarding is notoriously invasive and tedious, requiring grieving or elderly clients to hunt down decades of physical deeds, obscure insurance policy numbers, and outdated corporate registries. Shifting this burden to automated data extraction tools allows advisors to initiate estate conversations much earlier in the client lifecycle, transforming a morbid, back-office checklist into a collaborative, forward-looking family strategy.

However, the integration of autonomous agents into estate workflows introduces a delicate dance with the legal establishment. Bar associations and regulatory bodies have historically guarded the boundaries of estate law fiercely, routinely penalizing fintech platforms that cross the line from algorithmic document organization into unauthorized legal advice. To survive this scrutiny, modern platforms must position themselves strictly as collaborative infrastructure for financial professionals rather than direct-to-consumer legal engines. The goal is to prepare clean, pre-vetted asset maps that can be handed off to specialized estate attorneys, drastically reducing billable hours while keeping human compliance firmly in the driver's seat.

From an operational standpoint, the true metric of success for these AI-driven systems lies in their ability to handle highly fragmented, non-traditional asset classes. Today's modern estates no longer consist solely of blue-chip stocks, real estate holdings, and standard life insurance policies. Wealth managers are increasingly forced to account for complex digital footprints, ranging from monetized intellectual property and multi-jurisdictional business structures to highly volatile cryptocurrency portfolios and private equity stakes. Manually reconciling these disparate assets under evolving tax codes is an administrative nightmare that human compliance teams can no longer scale efficiently.

Ultimately, the digitization of legacy management marks a permanent shift in how the financial sector defines value. Wealth managers can no longer justify high fees purely through portfolio construction or basic market indexing, both of which have been thoroughly commoditized by automated robo-advisors. Instead, the competitive battlefield has moved toward holistic, hyper-localized family office services. Incorporating context-aware AI into estate planning allows mid-market advisory firms to offer the level of sophisticated, multi-generational wealth preservation that was once exclusively reserved for ultra-high-net-worth individuals.

The Fine Print on Autonomous Estate Planning

Reading Between the Lines: The industry’s sudden rush toward AI-driven estate planning rests on a highly fragile assumption: that automation can seamlessly replace human diligence in a sector governed by emotion, family politics, and bureaucratic chaos. Fintech startups eagerly pitch a world where specialized algorithms effortlessly untangle complicated family dynamics and archaic local tax codes. Yet, this glossy vision conveniently overlooks the stubborn reality of human behavior. No amount of advanced machine learning can force an estranged beneficiary to return a phone call, nor can an automated agent extract accurate asset details from a client who intentionally hides offshore accounts or forgotten properties from their financial advisor.

Furthermore, deploying automated systems into wealth management creates an interesting liability paradox. Software developers promise that algorithmic checks will catch costly compliance gaps and outdated beneficiary designations before they trigger tax penalties. However, when an autonomous system misinterprets a complex, multi-layered trust structure or fails to account for a minor amendment in a regional probate law, the question of legal culpability remains highly ambiguous. Financial advisors cannot simply point to an algorithm's hallucination to absolve themselves of fiduciary negligence, meaning firms will likely find themselves spending the time they saved on paperwork double-checking the machine's work line by line.

This tech-forward transition also highlights a blatant contradiction in how the financial sector views the next generation of clients. Wealth management firms are banking on AI tools to attract tech-savvy heirs who demand instant, digital-first experiences. At the exact same time, the industry acknowledges that estate planning is inherently an emotional, high-touch endeavor requiring immense empathy and interpersonal trust during moments of profound family grief. Attempting to bridge this gap with automated workflows risks turning a highly personalized milestone into an cold, transactional interface, potentially accelerating the very client abandonment that firms are desperately trying to prevent.

Looking ahead, the widespread democratization of these sophisticated wealth-structuring tools could inadvertently trigger a regulatory arms race. As automated platforms make it incredibly easy for mid-market clients to implement complex tax avoidance and asset protection strategies that were once exclusively reserved for billionaires, government tax authorities will almost certainly adapt. Regulatory bodies like the IRS or the CRA are highly unlikely to sit idly by while software automates the erosion of their tax base. It is highly probable that the widespread adoption of AI estate tools will simply push governments to deploy their own adversarial AI systems to audit and dismantle automated tax shelters in real time.

Ultimately, while AI agents will undoubtedly eliminate the mind-numbing administrative chore of scanning paper deeds and organizing files, they cannot automate the actual core of estate planning. True legacy management has never been a simple data-entry problem; it is an intimate exercise in human psychology, conflict resolution, and ethics. Tech platforms can successfully map out the exact distribution of a client's wealth, but they remain entirely blind to the delicate emotional landscape of the family receiving it. Until software can accurately predict how a sudden inheritance will impact family dynamics, the human advisor will remain the only component of the estate workflow that actually matters.

Leaving a lasting legacy used to require an army of expensive lawyers, a leather-bound binder, and a flair for family drama. Now, thanks to the magic of fintech innovation, we can delegate the existential dread of our own mortality to an automated software script—provided, of course, the AI doesn't accidentally leave the family vacation home to a completely hallucinated cousin.

Artūras Malašauskas is an AI Systems Integrator with 20+ years of production-grade web engineering experience. He has designed, shipped, and scaled enterprise Python/PHP systems for logistics, SaaS, and public-sector clients. For the past year, he has focused exclusively on AI integrations: deploying open-source LLMs, building generative media pipelines (image, audio, video), and engineering multi-agent workflows for real production environments. His standard: reproducibility, security, cost-efficient inference—no vaporware. He documents and evaluates emerging AI tooling, separating verified capabilities from marketing noise. Technical editor at: muza-ai.eu, ai-verslas.lt, ai-naujinos.lt Connect on LinkedIn

Comments