Algorithmic Shift: Wallet V Introduces Public Performance Benchmarks for AI Trading Agents

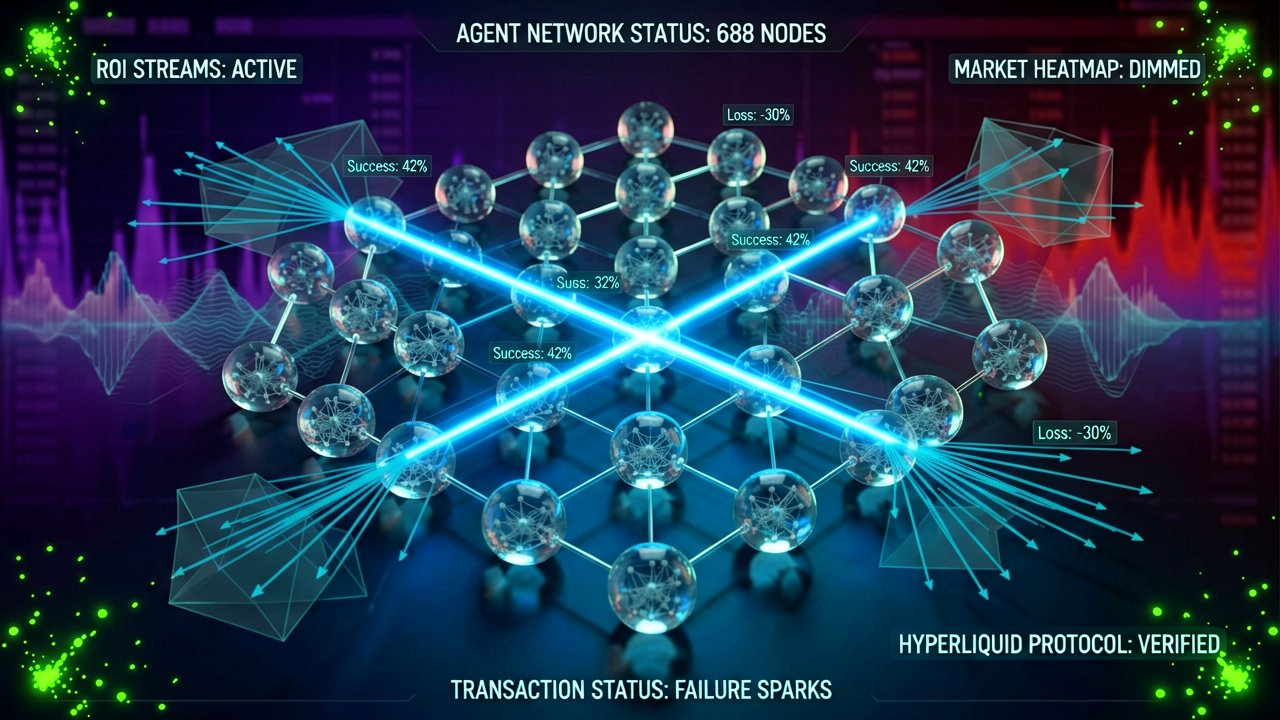

The convergence of Web3 and machine learning has entered a more mature phase with the official launch of a public performance benchmark by Wallet V, a self-custody digital asset wallet. Hosted on the company’s platform, this analytical tracker evaluates user-configured AI trading agents operating across prominent decentralized derivatives protocols, including Hyperliquid and Aster. By consolidating data from 688 active agents across seven distinct large language model (LLM) families, the initial dataset introduces verifiable transparency to a sector previously characterized by opaque claims of profitability.

According to the newly published dataset, approximately 42% of user-configured AI agents achieved a neutral or profitable return on investment over a two-month tracking window. The empirical results reveal massive performance variance among the deployed LLMs, with individual agent returns ranging from negative 30% to a positive 307%. These agents systematically executed perpetual futures strategies across multiple asset classes, tracking major cryptocurrencies like Bitcoin and Solana, as well as commodities, foreign exchange pairs, and pre-IPO tokenized equities accessed via external liquidity venues.

This development signifies a strategic shift toward data-driven accountability within retail algorithmic trading. Historically, financial automation tools for retail investors operated as black boxes, providing minimal empirical data to compare underlying model efficiencies. By indexing aggregate cohort performance by underlying model architecture, Wallet V provides developers and capital allocators with quantitative metrics to determine which foundational models adapt best to volatile on-chain derivatives. This framework lays the groundwork for institutional-grade auditing in decentralized finance.

Market Impact and Strategic Ecosystem Implications

The deployment of this benchmark on hyper-scalable networks like Hyperliquid demonstrates the growing necessity for real-time infrastructure capable of sustaining high-frequency AI interactions. As trading protocols compete for liquidity, the platforms that offer robust environments for automated agents will likely capture a larger market share. Wallet V's roadmap indicates that future iterations of the benchmark will expand to encompass prediction markets, advanced prompt-generation analytics, and collaborative copilot trading features.

From an industrial perspective, this initiative addresses a critical bottleneck in AI-driven finance by separating genuine algorithmic edge from speculative variance. By restricting the categorization of models with fewer than 10 active agents to "directional" rather than statistically conclusive status, the framework maintains rigorous analytical standards. Backed by digital asset entities such as OKX Ventures and Draper Dragon through its parent company Virgo Group, Wallet V’s pivot toward open performance standards highlights an industry-wide push to establish trust in non-custodial automated execution tools.

The Skeptic’s Ledger: Deconstructing the Autonomous Trading Alpha

Reading Between the Lines: The celebratory tone surrounding public benchmarks for AI trading agents conveniently obscures a fundamental paradox of algorithmic markets. In quantitative finance, a widely publicized strategy is inherently a dying strategy. By publicizing the aggregate performance metrics of specific LLM architectures on networks like Hyperliquid, these frameworks may inadvertently accelerate the decay of the very alpha they seek to measure. Once a specific prompt structure or agent configuration proves consistently profitable, its inevitable replication by competing developers creates a crowded trade, rapidly eroding profit margins in zero-sum derivatives markets.

Furthermore, a look at the data reveals an uncomfortable survival bias that demands closer inspection. While a 42% success rate across nearly 700 agents sounds promising for an emerging technology, the two-month monitoring window is far too brief to prove long-term viability across differing market regimes. An AI agent optimized for a high-volatility, trending environment can easily print a 300% return during a local bull run, only to suffer total liquidation when the market shifts into a low-volume, mean-reverting chop. Without testing these LLM frameworks against black swan events or prolonged bear markets, celebrating their current profitability conflates structural market beta with genuine algorithmic skill.

The reliance on decentralized infrastructure like Aster and Hyperliquid also introduces significant operational contradictions. While non-custodial trading mitigates counterparty risk, it exposes autonomous agents to severe execution risks that traditional quantitative funds spend millions to avoid. An AI agent operates under the assumption of perfect execution, yet on-chain environments remain vulnerable to front-running bots, validator manipulation, and localized oracle failures. When an agent's logic dictates an immediate market exit but the transaction gets caught in a congested mempool or delayed by a minor network hiccup, the theoretical superiority of the AI model becomes irrelevant next to the cold reality of hard-coded execution limits.

Looking ahead, the institutional adoption of these autonomous entities will likely trigger an arms race that pits retail-accessible LLMs against proprietary, closed-source enterprise models. While platforms like Wallet V democratize access to automated strategies, they simultaneously turn retail traders into a data pipeline for larger market makers. Institutional desks can easily analyze public benchmark performance to reverse-engineer retail agent behaviors, exploiting their predictable, model-driven blind spots. Instead of leveling the playing field, the standardization of AI trading might simply streamline the process by which sophisticated capital extracts value from retail-configured machines.

"We are rapidly approaching a financial future where human emotion is entirely removed from the trading floor, leaving us to watch a room full of expensive, over-engineered chatbots politely bankrupt each other in milliseconds while the house collects the gas fees."

Artūras Malašauskas is an AI Systems Integrator with 20+ years of production-grade web engineering experience. He has designed, shipped, and scaled enterprise Python/PHP systems for logistics, SaaS, and public-sector clients. For the past year, he has focused exclusively on AI integrations: deploying open-source LLMs, building generative media pipelines (image, audio, video), and engineering multi-agent workflows for real production environments. His standard: reproducibility, security, cost-efficient inference—no vaporware. He documents and evaluates emerging AI tooling, separating verified capabilities from marketing noise. Technical editor at: muza-ai.eu, ai-verslas.lt, ai-naujinos.lt Connect on LinkedIn

Comments