The cybersecurity landscape is shifting beneath our feet, and Zscaler is attempting to position itself directly at the epicenter of this transformation. By aggressively expanding its Zero Trust Exchange platform into dedicated artificial intelligence security suites, the cloud pioneer is answering an undeniable market demand. However, this sprint toward innovation has exposed an increasingly familiar tension on Wall Street: the gap between a tech company’s long-term product vision and investors' immediate hunger for hyper-growth and margin expansion.

Recent data underscores the sheer velocity of the problem Zscaler is trying to solve. According to the company's Zscaler 2026 AI Security Report, global enterprise AI/ML transactions spiked a staggering 83% year-over-year, leaving a massive oversight gap where sensitive corporate data is regularly exposed to unverified public LLMs. While CEO Jay Chaudhry positions his company as an essential tollbooth for autonomous AI agents, shareholders are carefully tracking the high sales and marketing investments required to evangelize these sophisticated, multi-pillar defense platforms.

The Execution Reality Versus Valuation Pressures

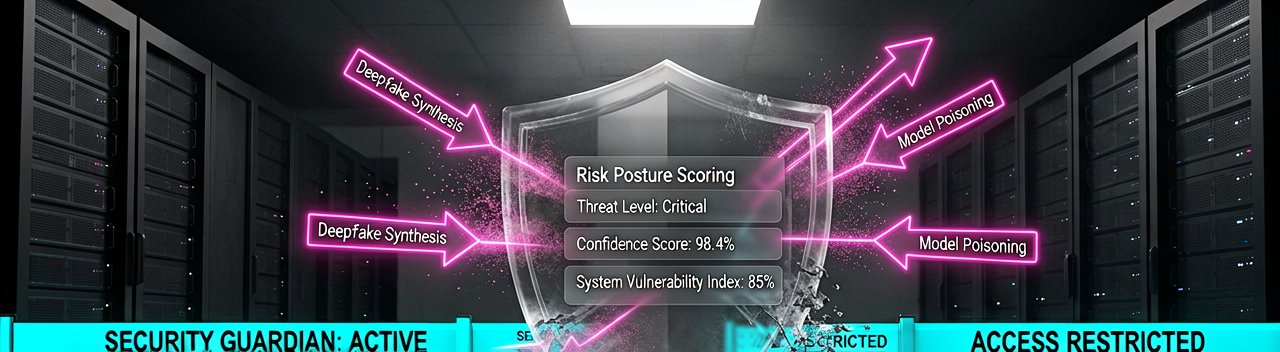

What most reports miss is that Zscaler is playing a fundamentally different game than the point-product vendors it frequently replaces. The enterprise reality is a double-edged sword; organizations are racing to adopt generative AI tools, yet safety concerns have forced companies to block nearly 39% of that traffic entirely. Zscaler's new AI Security Suite aims to bridge this chasm by offering granular asset management, risk posture scoring, and runtime guardrails. It is an impressive technological flex, but converting security anxiety into immediate enterprise-wide contract expansions takes time, especially as clients look to consolidate their overall software spending.

Financially, Zscaler is far from faltering, yet it sits under a microscope. In its latest quarterly update, the vendor delivered a strong 26% revenue increase to $815.8 million, easily outpacing many legacy competitors as noted in market roundups by Yahoo Finance. The company even boosted its full-year fiscal outlook, forecasting annual recurring revenue up to $3.745 billion. Despite hitting a remarkable "Rule of 62" when combining revenue growth and free cash flow margins, the stock's valuation multiples have compressed, reflecting a broader market debate over whether AI native security tools might eventually disintermediate cloud-native architectures.

Balancing Autonomous Defense and Enterprise Budget Caps

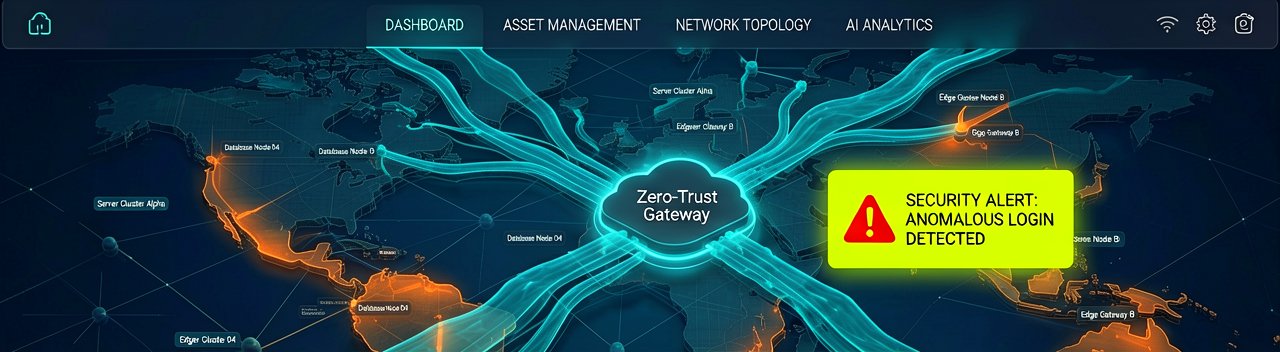

Behind the scenes, the long-term bullish case for Zscaler hinges on the impending transition from human-driven workflows to fully autonomous agentic AI. As cyber attackers deploy machine-speed exploits, traditional security perimeters become obsolete, reinforcing the necessity of an inline, zero-trust cloud architecture. Zscaler's strategic roadmap relies on its security cloud intercepting and analyzing close to a trillion transactions to train its own defensive algorithms, establishing a massive data moat that smaller startups simply cannot replicate overnight.

The short-term hurdle remains tactical execution. Enterprise buyers are exhausted by cybersecurity fragmentation, yet their budgets are tightly capped by macroeconomic realities. To justify premium valuations, Zscaler must prove that its new AI features can dramatically expand revenue per existing customer without forcing a parallel surge in customer acquisition costs. Until these high-margin AI suites move from early-adopter proof-of-concepts to standard enterprise deployments, the uneasy standoff between visionary tech roadmap planning and rigid quarterly earnings expectations will likely persist.

The Architecture Paradox and Corporate Caution

Reading Between the Lines: There is a deep, structural irony in the way the cybersecurity market currently values "AI-native" innovation. Wall Street routinely punishes vendors for spending too heavily on research and development, yet it simultaneously threatens to penalize them with lower valuation multiples if they fail to out-innovate the latest crop of venture-backed startups. Zscaler finds itself trapped in this specific loop, forced to constantly spend to validate its legacy cloud footprint while building an entirely new defense engine for an era of autonomous software agents that most enterprises have not even fully deployed yet.

This dynamic reveals a fundamental friction between theoretical threat vectors and actual corporate purchasing behavior. While security vendors paint alarming pictures of rogue AI bots executing lightning-fast exploits, the chief information security officers signing the checks are often more preoccupied with mundane configuration errors and employee password hygiene. Zscaler is marketing an advanced, high-margin umbrella for a digital thunderstorm that many corporate legal and compliance departments are deliberately trying to avoid by restricting employee access to generative tools in the first place.

Furthermore, the long-term assumption that massive transaction volume translates into an unassailable data moat deserves a healthy dose of skepticism. Having an inline cloud architecture that processes hundreds of billions of daily data logs is only half the battle. If the underlying data is largely composed of repetitive, low-value employee queries to public search engines, the cost of storing, parsing, and cleaning that information could easily outpace the actual monetization value of the resulting security modules, squeezing margins at the exact moment investors expect efficiency gains.

Ultimately, the industry is witnessing a classic transition phase where software capabilities have temporarily outrun market readiness. Zscaler's tech stack is undeniably prepared for a world where AI agents talk exclusively to other AI agents across decentralized networks. The catch is that human-centric legacy applications still dominate the enterprise landscape, leaving Zscaler to fund a costly, forward-looking security apparatus while relying on old-school billing structures to satisfy a highly impatient, quarter-to-quarter financial crowd.

In the modern tech sector, the ultimate corporate balancing act is convincing your engineers that you are building the digital shield of the twenty-first century, while convincing your institutional shareholders that you are running a tight, boring utility company that never spends an extra dollar on a rainy day.

Artūras Malašauskas is an AI Systems Integrator with 20+ years of production-grade web engineering experience. He has designed, shipped, and scaled enterprise Python/PHP systems for logistics, SaaS, and public-sector clients. For the past year, he has focused exclusively on AI integrations: deploying open-source LLMs, building generative media pipelines (image, audio, video), and engineering multi-agent workflows for real production environments. His standard: reproducibility, security, cost-efficient inference—no vaporware. He documents and evaluates emerging AI tooling, separating verified capabilities from marketing noise. Technical editor at: muza-ai.eu, ai-verslas.lt, ai-naujinos.lt Connect on LinkedIn

Comments