The Automated Adversary: How the AI Scam Boom Unraveled Modern Digital Defenses

The traditional rules of digital self-defense have officially dissolved. For years, security professionals gave consumers a reliable checklist to spot fraud: look for bad grammar, awkward phrasing, and suspicious sender addresses. But over the last year, cybercriminals weaponized generative artificial intelligence to industrialize deception, launching highly tailored, flawless attacks that mimic legitimate institutions and loved ones with terrifying accuracy. This rapid evolution has caught both everyday consumers and global financial organizations off guard, transforming fraud from an occasional nuisance into an institutional crisis.

According to comprehensive data compiled by the Federal Trade Commission, imposter scams skyrocketed into the leading category of fraud reports, fleecing victims out of a staggering $3.5 billion in losses. The explosion in sophisticated cyber fraud caught the attention of federal authorities, prompting formal tracking of artificial intelligence's footprint in financial crimes. Concurrently, the Federal Bureau of Investigation's Internet Crime Complaint Center documented over 22,000 explicit AI-related fraud complaints, resulting in close to $900 million in damages. The numbers reflect a broader structural shift; cybercrime networks are no longer relying on clumsy, manually distributed phishing emails, choosing instead to deploy cheap, automated tools capable of scaling operations globally in seconds.

The Evolving Weaponry of Digital Impersonation

At the center of this criminal renaissance is the alarming refinement of voice cloning and deepfake software. Bad actors need as little as three seconds of audio, often scraped from a public social media video, to replicate an individual’s voice perfectly. These clones power highly manipulative family-imposter schemes, where panicked relatives receive realistic distress calls demanding urgent wire transfers. Because the psychological shock of hearing a loved one in trouble overrides critical thinking, these voice-cloned attacks net significantly higher payouts per victim than outdated text-based scams.

The deception doesn't stop at personal relationships. Global fraud syndicates are aggressively targeting investors by running AI-generated video advertisements featuring deepfaked politicians and prominent corporate executives. These highly polished videos steer unsuspecting targets toward fraudulent trading platforms, a trend that saw investment fraud metrics surge globally. Beyond consumer-facing deceit, criminals use generative tools to forge hyper-realistic documentation and synthetic identities, effectively tricking bank onboarding systems and bypassing static identity verification controls.

Banks and Regulators Scramble to Rebuild Defenses

For financial institutions, the realization that legacy defense mechanisms are fundamentally reactive has sparked an aggressive technological pivot. Relying on static, event-based rules to flag suspicious activity is no longer viable when AI-driven transactions blend seamlessly into legitimate user behaviors. To counter this, major banks are rushing to integrate behavioral biometrics and real-time device intelligence capable of detecting subtle, anomalous patterns during a live session. A report detailing global payment security trends from Mastercard noted that while generative tools fuel billions in potential losses, defensive AI models have already successfully saved specific card issuers millions by automating smarter, instantaneous authorization decisions.

Regulators are similarly turning up the heat on the tech sector. The Federal Trade Commission issued stern warnings to platforms and developers, emphasizing that the agency is actively scrutinizing companies that deploy deceptive AI tools or make unsupported claims about their security capabilities. Furthermore, policy updates indicate that federal enforcement will aggressively penalize entities that knowingly facilitate or turn a blind eye to fraudulent automation on their networks. As cross-border cyber fraud networks expand, security experts emphasize that stopping the bleed will require unprecedented data sharing between financial institutions, telecom providers, and international law enforcement agencies.

Behind the Scenes: The Underground Economies Fueling the Fraud Machine

What most public reports miss is that the surge in artificial intelligence scams is not driven by lone-wolf hackers working in isolation, but by a highly organized, commercialized corporate structure in the digital underground. Cybercrime syndicates have effectively industrialized fraud by offering "Fraud-as-a-Service" (FaaS) platforms on dark web marketplaces. For a nominal monthly subscription fee, even low-skilled operators can rent pre-configured large language models stripped of safety rails, custom voice-cloning engines, and automated deployment bots. This commercialization has drastically lowered the barrier to entry, allowing local criminal rings to execute global, state-of-the-art cyber campaigns that previously required nation-state capabilities.

The operational pivot of these syndicates mirrors the efficiency of modern tech startups. These underground networks recruit developers to continuously refine deepfake algorithms, optimizing them to bypass specific facial recognition and identity verification systems used by major digital wallets and crypto exchanges. They maintain dedicated quality assurance teams to test fraudulent scripts against current banking filters. By treating cyber fraud as an agile business model, syndicates can iterate their code within hours of a bank deploying a security patch, ensuring their malicious tools remain highly effective against traditional defenses.

From the perspective of frontline banking security executives, this shift represents a fundamental asymmetry in modern warfare. While financial institutions must secure millions of accounts across varied legacy platforms, a fraud operator only needs to find a single entry point or exploit a few seconds of audio to succeed. Security teams are increasingly vocal about the psychological toll this environment takes on human fraud analysts, who must constantly evaluate complex, high-stakes incidents where the line between a genuine customer and a deepfaked identity has completely blurred. This psychological fatigue within security operations centers has itself become a vulnerability that syndicates actively exploit.

Historically, fraud prevention relied heavily on educated consumer skepticism and the assumption that digital media was inherently trustworthy. The sudden democratization of generative media tools completely upends this societal trust architecture, creating a reality where video and audio evidence are no longer definitive proof of identity. Industry historians note that this transition is reminiscent of the early days of email phishing, but accelerated tenfold due to the rapid scaling power of cloud computing. The absolute erosion of digital trust forces organizations to move away from verifying who a person claims to be based on static data, shifting instead toward continuous verification based on how they behave online.

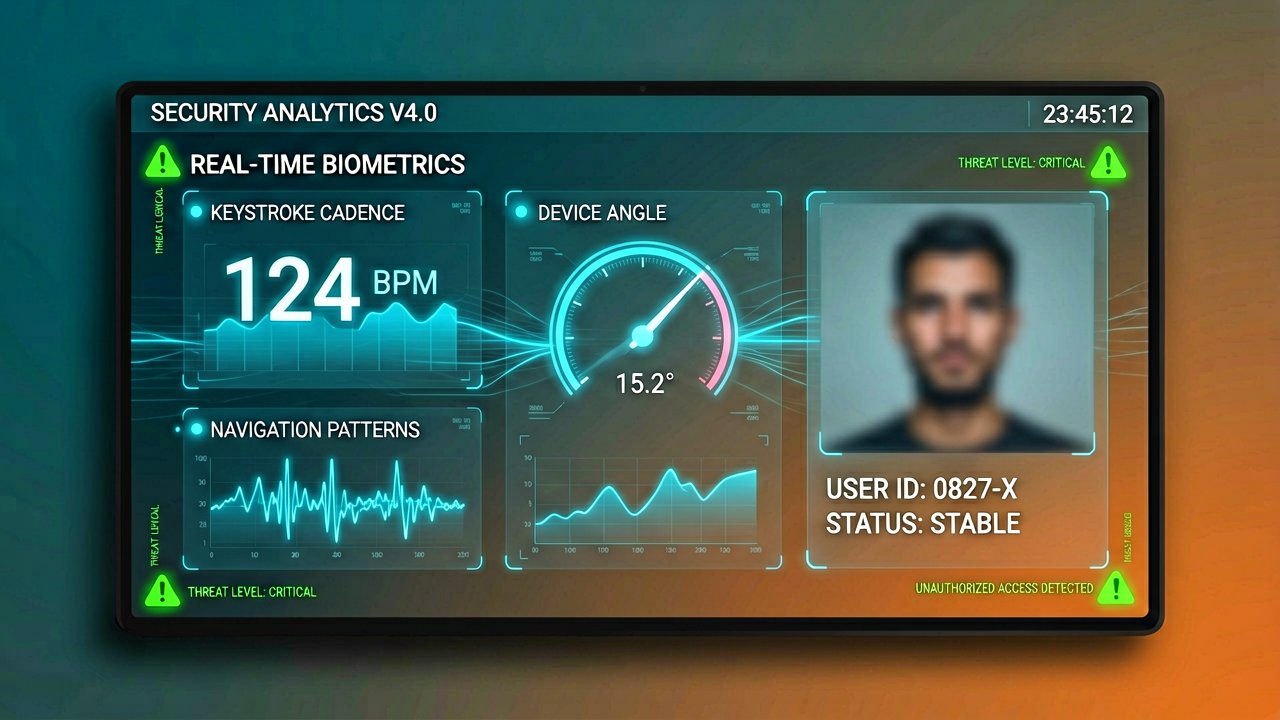

To survive this environment, forward-looking financial institutions are fundamentally rewriting their risk models. They are moving away from relying on single-factor confirmations, such as one-time passwords sent via text, which are easily intercepted or social-engineered away by AI bots. Instead, defenses are shifting toward silent, ambient security measures like analyzing the specific cadence of a user's keystrokes, the angle at which they hold their mobile device, and their natural navigation patterns. By focusing entirely on these uncopiable human traits, institutions hope to build an adaptive perimeter capable of neutralizing automated adversaries before a single dollar leaves an account.

Reading Between the Lines: The Fallacy of the Perfect Algorithmic Shield

The prevailing narrative pushed by fintech marketing departments suggests that the antidote to artificial intelligence fraud is simply more artificial intelligence. This comforting premise assumes that a more sophisticated algorithm can neatly patch the vulnerabilities exposed by another. However, this logic ignores a fundamental contradiction: defensive models are bound by strict regulatory constraints, data privacy laws, and corporate risk tolerances, whereas offensive models operate entirely without boundaries. By treating this crisis as a purely technical problem to be solved with software updates, institutions are engaging in a costly game of whack-a-mole that fails to address the underlying vulnerability, which remains stubbornly human.

Furthermore, the push toward continuous behavioral monitoring and ambient biometric tracking introduces a delicate trade-off between absolute security and consumer privacy. To effectively flag a deepfaked identity or a machine-generated transaction, banks must ingest unprecedented amounts of granular user data, tracking everything from a customer’s typing speed to their physical location. This creates a deeply ironic security paradox. The massive repositories of behavioral data harvested to protect consumers inevitably become high-value targets for the next generation of cybercriminals, who can use stolen biometric profiles to train even more precise, unmaskable synthetic personas.

Projecting into the near future, the rapid proliferation of automated fraud will likely widen the digital divide, disproportionately impacting vulnerable populations who lack the technical literacy to navigate a hyper-paranoid digital ecosystem. As financial institutions implement increasingly friction-heavy authentication hurdles to weed out sophisticated bots, the everyday banking experience risks becoming hostile to the average user. If the price of a secure transaction is a multi-layered gauntlet of biometric scans and behavioral challenges, the industry may inadvertently alienate the very consumers it is scrambling to protect, trading seamless utility for a fortress of digital paranoia.

"We have spent decades building a digital world where convenience is king and connectivity is absolute, only to discover that we inadvertently constructed the perfect playground for automated grifters. In the end, the ultimate defense against a multi-million-dollar generative AI scam isn't a smarter algorithm—it is the deeply untechnological willingness to hang up the phone, take a breath, and call your grandmother back on a verified number."

Artūras Malašauskas is an AI Systems Integrator with 20+ years of production-grade web engineering experience. He has designed, shipped, and scaled enterprise Python/PHP systems for logistics, SaaS, and public-sector clients. For the past year, he has focused exclusively on AI integrations: deploying open-source LLMs, building generative media pipelines (image, audio, video), and engineering multi-agent workflows for real production environments. His standard: reproducibility, security, cost-efficient inference—no vaporware. He documents and evaluates emerging AI tooling, separating verified capabilities from marketing noise. Technical editor at: muza-ai.eu, ai-verslas.lt, ai-naujinos.lt Connect on LinkedIn

Comments