The GPU Diet: How BC Card is Trimming AI Infrastructure for the Agentic Era

In a move that’s sending ripples through both the fintech and silicon sectors, South Korean payment giant BC Card has just pulled back the curtain on its "Agentic AI Operation Platform" during a high-profile debut in the United States. While the tech world is currently obsessed with chatbots that can merely "chat," BC Card is pivoting toward agents that can actually "do." The headline-grabbing kicker? This new architecture reportedly slashes GPU resource usage by a staggering 70% compared to traditional large-scale model deployments.

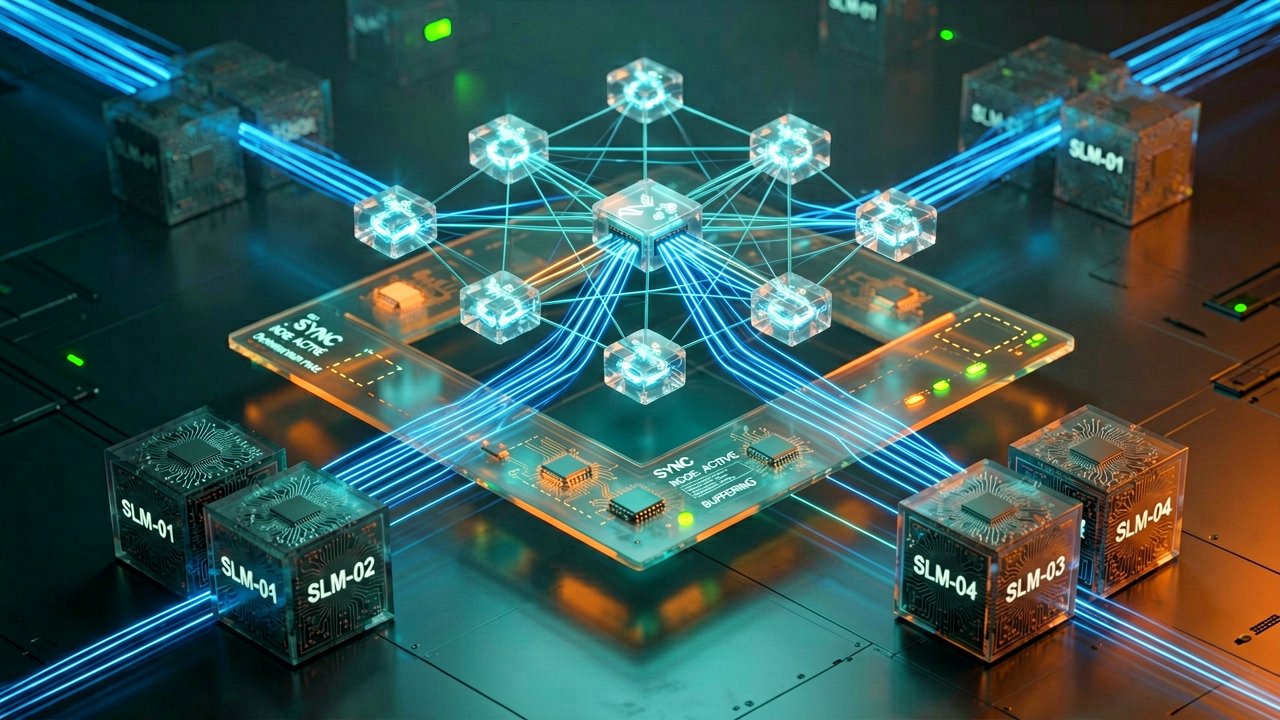

It’s no secret that the AI boom has put a massive strain on the global supply of graphics processing units (GPUs). For financial institutions processing billions of transactions, the cost of running a massive LLM (Large Language Model) for every single query is essentially a ticket to bankruptcy. BC Card’s solution, according to a recent report by The Asia Economy Daily, involves a clever shift: clustering multiple Small Language Models (SLMs) instead of relying on one bloated, general-purpose giant.

The Secret Sauce: Efficiency Through Specialization

The logic here is refreshingly pragmatic. Instead of asking a $30,000 GPU to handle every mundane task, BC Card’s platform assigns specialized SLMs to specific domains—like restaurant recommendations or internal workflow support. By orchestrating these smaller, leaner models, they’ve managed to triple inference speeds while keeping their hardware budget from spiraling out of control. It’s a classic "work smarter, not harder" approach that treats AI as a precise tool rather than a blunt instrument.

This isn't just a lab experiment. BC Card is already putting this tech to work through a trio of services showcased at the event. There’s "Eat.pl," which uses real-time consumption patterns to play restaurant matchmaker; "BCGPT," a finance-tailored generative AI for employees; and "MOAI," an automation engine that stitches multiple AIs together to handle complex tasks. It's clear they’re looking to prove that "agentic" means more than just a buzzword—it means autonomy with an eye on the bottom line.

The timing of this US unveil is particularly poignant given the broader industry shift. We’re seeing a radical rethink of how data centers are built. As noted by analysts at AMD, the era of "chatbot AI" favored a lopsided 1:8 CPU-to-GPU ratio. But agentic AI requires heavy-duty orchestration—tasks like planning, tool-calling, and reasoning—which are increasingly pushing that ratio toward 1:1, or even favoring the CPU for logic-heavy workloads.

The Global Race for the "Agentic" Standard

BC Card isn't the only one trying to plant a flag in this territory. In the last few weeks alone, we've seen Anthropic launch agents designed for Wall Street pitch decks and Mastercard roll out an "Agent Suite" for its ecosystem. The competition is fierce because the stakes are enormous; Boston Consulting Group projects that agentic AI could influence over $1 trillion in e-commerce spending in the coming years.

What sets BC Card apart in this scrum is its focus on the "how." While others are focused on the front-end user experience, BC Card is tackling the infrastructure bottleneck. By proving you can get high-tier financial "intelligence" without a 70% larger power bill, they’re positioning themselves as a vital player for any enterprise that wants to scale AI without melting their servers or their bank accounts.

Ultimately, BC Card’s US debut signals a shift from the "experimental" phase of AI to the "operational" one. It’s a world where agents don't just suggest a gift for your spouse; they find it, verify the merchant's security, and process the payment—all while running on a lean, optimized hardware stack. If they can truly deliver on that 70% reduction in GPU reliance, the rest of the industry is going to have to catch up fast.

Would you like to explore the specific architecture behind their SLM clustering, or should we look into how other major card issuers are responding to this efficiency breakthrough?

The Hidden Architecture of Efficiency

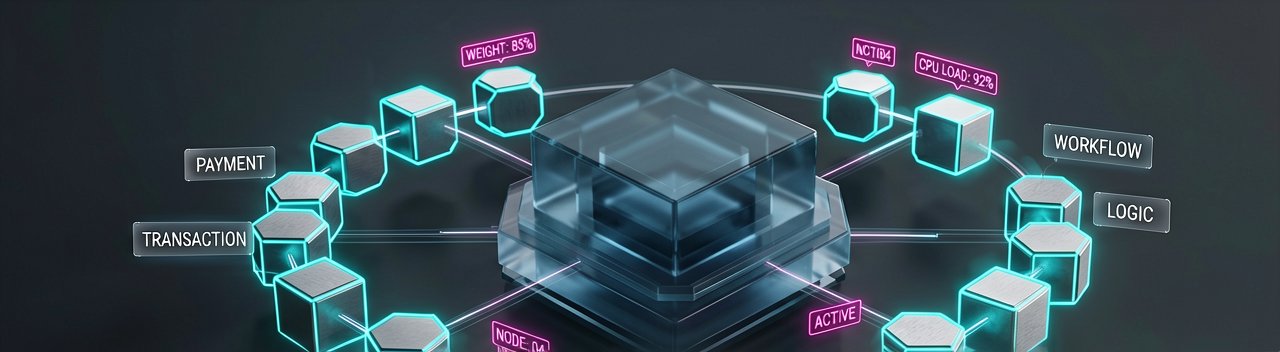

What Most Reports Miss: The real genius behind BC Card’s 70% GPU reduction isn’t just about using "smaller" models; it’s about a fundamental shift in how a financial engine thinks. In the traditional AI paradigm, we’ve been throwing massive, 175-billion-parameter models at every problem, the computational equivalent of using a Boeing 747 to deliver a pizza. BC Card’s "Agentic AI Operation Platform" essentially builds a fleet of specialized delivery bikes. By utilizing a "Router" layer that analyzes a query’s intent before it ever hits the silicon, the system directs traffic to specific Small Language Models (SLMs) that have been fine-tuned on nothing but payment data and merchant metadata.

This "Model-as-a-Service" (MaaS) approach reflects a hard-learned lesson from the early days of South Korean fintech. Historically, Korean financial giants like BC Card’s parent, KT Corporation, have struggled with the massive overhead of localized cloud infrastructure. By moving toward agentic orchestration, they aren't just saving on energy; they are solving the latency problem. When an agent can process a request on a local SLM without waiting for a massive cloud-based LLM to "reason" through a simple transaction check, the user experience shifts from "clunky chatbot" to "instant assistant."

Industry insiders suggest that this move is a direct defensive play against the encroaching "Big Tech" shadow. With Apple and Google integrating financial layers directly into their operating systems, traditional card issuers are terrified of becoming "dumb pipes." BC Card is betting that by owning the orchestration layer—the "brain" that decides which model does what—they can maintain a proprietary grip on the transaction lifecycle. It’s a sophisticated play to stay relevant in an era where the credit card in your wallet is becoming less important than the AI agent in your phone.

The Hardware-Software Divorce

Historically, finance tech has been tethered to specific hardware cycles, but this new platform suggests a decoupling. By optimizing for 70% less GPU usage, BC Card is essentially "future-proofing" itself against the next semiconductor shortage. If you don't need the latest H100 or Blackwell chips to run a world-class financial agent, you aren't beholden to Nvidia’s supply chain. This is music to the ears of CFOs who have watched their AI R&D budgets balloon over the last twenty-four months.

From a stakeholder perspective, the "Eat.pl" and "MOAI" services are more than just apps; they are data harvesters. Every time a user interacts with these agents, the platform learns more about the nuances of "agentic failure"—those moments when an AI loses the thread of a task. BC Card’s leadership has hinted that the long-term goal is to export this platform as a white-label solution for smaller banks across Southeast Asia and the US who can't afford their own AI divisions but desperately need to automate their back-office workflows.

Ultimately, this US debut serves as a "shot across the bow" for Silicon Valley. It proves that the next great leap in AI might not come from a lab in San Francisco, but from a payment processor in Seoul that simply had to find a way to make the numbers work. As we move into an era of "sovereign AI," where companies and nations want to control their own models, BC Card’s lean, agentic framework offers a blueprint for how to scale intelligence without breaking the power grid.

Would you like to analyze the competitive landscape of SLM orchestration among other "Big Three" credit providers, or shall we dig into the specific data privacy implications of these autonomous financial agents?

Reading Between the Lines: The Cost of Autonomy

The 70% efficiency metric is a seductive headline, but a healthy dose of skepticism is required when assessing the "agentic" revolution. In the tech world, efficiency gains of this magnitude often come with a hidden tax—usually in the form of accuracy or "hallucination" overhead. While BC Card’s SLM clustering approach minimizes the electrical bill, it introduces a complex orchestration challenge: the "Telephone Game" effect. When multiple specialized models pass data back and forth to complete a single financial task, the risk of a logic breakdown increases exponentially compared to a single, monolithic intelligence.

There is also a glaring contradiction in the industry’s push for "agentic" independence. We are told these systems will operate with minimal human oversight to save costs, yet the financial sector remains one of the most heavily regulated environments on Earth. If an autonomous agent like MOAI makes an unauthorized "hallucinated" transaction or fails to flag a sophisticated laundering pattern because it was optimized for speed over depth, the 70% savings on GPU hardware will be quickly eclipsed by 100% of a regulatory fine. BC Card is walking a tightrope between lean operations and the rigid "black box" problem that still plagues small-model architectures.

Furthermore, the move to the US market isn't just about showing off tech; it’s a strategic gamble on data interoperability. US financial data is notoriously siloed compared to the more integrated digital landscape in South Korea. For BC Card’s agents to truly shine, they need deep access to consumer behavior that American banks are historically loath to share. Without that "data fuel," the most efficient GPU engine in the world is just a very fast car idling in a driveway. The real test won't be the inference speed of their chips, but the willingness of the American financial ecosystem to let a foreign agent hold the keys to the vault.

Finally, we have to consider the labor implications that the press releases gloss over. "Agentic AI" is, at its core, a replacement for middle-tier analytical roles. While BC Card frames this as "empowering employees," the long-term projection for a platform that triples inference speed and automates complex workflows is a significantly smaller headcount. The industry is currently cheering for the "GPU reduction," but the "Human reduction" is the variable that few in the C-suite are ready to discuss publicly. As these agents become more autonomous, the line between a "tool for employees" and a "replacement for the department" becomes increasingly blurry.

"We’ve spent decades teaching humans to act like efficient machines, only to realize it’s much cheaper to just buy the machines—assuming, of course, you can find enough electricity to keep the 'agents' from taking a permanent coffee break."

Artūras Malašauskas is an AI Systems Integrator with 20+ years of production-grade web engineering experience. He has designed, shipped, and scaled enterprise Python/PHP systems for logistics, SaaS, and public-sector clients. For the past year, he has focused exclusively on AI integrations: deploying open-source LLMs, building generative media pipelines (image, audio, video), and engineering multi-agent workflows for real production environments. His standard: reproducibility, security, cost-efficient inference—no vaporware. He documents and evaluates emerging AI tooling, separating verified capabilities from marketing noise. Technical editor at: muza-ai.eu, ai-verslas.lt, ai-naujinos.lt Connect on LinkedIn

Comments