OpenAI Taps Plaid to Turn ChatGPT into Your New Personal Accountant

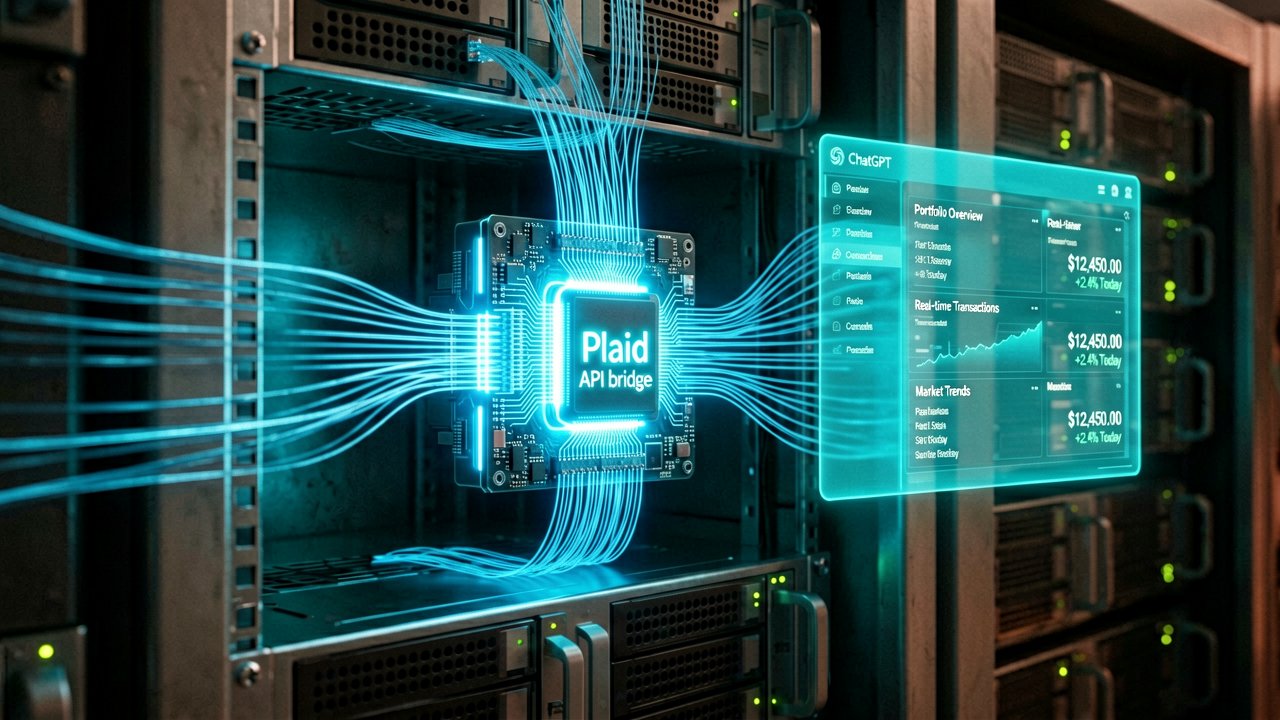

OpenAI is moving past the era of generic budgeting tips and "hallucinated" math. By integrating Plaid directly into ChatGPT Pro, the company is finally giving its AI a real-world tether to your actual wallet. Starting today, Pro subscribers in the U.S. can link their bank accounts, credit cards, and investment portfolios to the chatbot, effectively transforming a text-based assistant into a live financial dashboard. According to the official announcement from OpenAI, this new experience allows users to track spending, monitor subscriptions, and even check portfolio performance through a dedicated "Finances" sidebar or by simply tagging @Finances in a chat.

The tech behind this move is as much about trust as it is about data. By partnering with Plaid, OpenAI avoids the security nightmare of handling raw bank login credentials directly. Instead, Plaid acts as the secure bridge to over 12,000 financial institutions, including heavyweights like Chase, Fidelity, and Robinhood. It’s a calculated play; OpenAI notes that 200 million people already ask ChatGPT for financial advice every month. By grounding those conversations in real-time transaction data rather than just training-set theory, the AI can finally answer "Can I afford that vacation?" with something more substantial than a shrug and a "maybe."

The "Read-Only" Guardrails and What Comes Next

Don't expect ChatGPT to start paying your bills just yet. This integration is strictly read-only, meaning the AI can look at your data to provide insights and visualization but cannot move a single cent. It's a conservative starting point that likely aims to soothe the privacy jitters that inevitably come when you let a silicon brain peek at your credit card statement. Reporting from TechCrunch highlights that this feature was accelerated by OpenAI’s recent acquisition of the Hiro team, a personal finance startup that clearly had the blueprint for this kind of integration ready to go.

Looking ahead, the roadmap seems to involve even deeper ecosystem ties. OpenAI has already teased upcoming support for Intuit, which could eventually bring tax-impact analysis and credit approval predictions into the mix. For now, users can disconnect their accounts at any time through their settings, and OpenAI promises that any synced data is wiped within 30 days of removal. It’s a bold step toward making AI a functional utility rather than just a conversational novelty, provided you’re comfortable with the "all-seeing eye" knowing exactly how much you spent on takeout last Tuesday.

The Strategy Behind the Ledger

The Bigger Picture: This isn't just about making ChatGPT a better calculator; it’s a strategic land grab for the most valuable data silo remaining in the consumer tech space. While Google and Apple have long dominated the payment rail through digital wallets, OpenAI is positioning itself to own the logic layer above those transactions. By integrating Plaid, OpenAI is essentially building an operating system for life management where the AI doesn't just know what you say, but what you actually do with your capital. It’s a move that mirrors the early days of Mint.com, but with the added muscle of a Large Language Model that can synthesize thousands of line items into a coherent narrative in seconds.

Industry veterans see this as the "Hiro Effect" finally manifesting. When OpenAI quietly scooped up the team behind the finance app Hiro, the speculation was that they wanted to solve the "grounding" problem—the tendency for AI to make up numbers when it lacks a direct data source. According to analysis by The Verge, the Hiro acquisition provided the specialized infrastructure needed to handle the messy, fragmented world of banking APIs. This integration suggests OpenAI is moving away from being a general-purpose oracle and toward a suite of specialized, high-utility tools that can compete with dedicated fintech software.

There is also a significant competitive dimension to consider regarding the "agentic" future of AI. For an AI agent to truly act on a user's behalf, it needs access to their resources. By establishing this read-only link now, OpenAI is training its user base to trust the model with sensitive financial permissions. Stakeholders at Plaid have noted that the integration uses the OAuth standard, ensuring that ChatGPT never actually sees a user’s username or password. This layer of abstraction is critical for institutional adoption, as banks are notoriously protective of their moats and wary of any third-party interface that could lead to credential harvesting or fraud.

From a product perspective, the nuance lies in how ChatGPT handles "hallucination" in a financial context. OpenAI has implemented a specific verification layer for the @Finances tool, which prioritizes retrieved data over generated text. If the AI is asked about a balance, it is programmed to query the Plaid API directly and present that raw data rather than attempting to "predict" what the balance might be based on previous context. This shift from generative to retrieval-augmented generation (RAG) is the technical backbone that makes the feature viable for something as high-stakes as personal accounting.

Finally, the timing of this launch coincides with a broader shift in the fintech landscape toward "Open Banking" regulations in the U.S. and Europe. As regulators push for more consumer control over financial data, OpenAI is stepping in to be the primary interface for that data. While traditional banks have struggled to build intuitive apps that people actually enjoy using, OpenAI is betting that users would rather talk to a chatbot about their spending habits than navigate a labyrinth of banking menus. It’s a gamble on the "conversational interface" being the ultimate aggregator for our digital lives.

The Friction Between Privacy and Utility

Reading Between the Lines: While OpenAI and Plaid are framing this as a win for consumer empowerment, the reality is a paradoxical trade-off between privacy and personal insight. We are essentially being asked to believe that the world’s most data-hungry AI can sit atop our entire financial history without "learning" from the patterns it sees. Although OpenAI insists that data from the Plaid integration isn't used to train its foundational models, the history of "anonymized" data suggests that true separation is often a technical ideal rather than a practical reality. The sheer granularity of transactional data—where you eat, what medicine you buy, and which political causes you support—creates a profile far more intimate than any chat log ever could.

There is also the uncomfortable contradiction of "read-only" safety. While a read-only bridge prevents the AI from draining a savings account in a fit of digital confusion, it also highlights the current limitations of AI "agents." If the tool can identify an overpriced subscription but cannot actually cancel it, it remains a high-tech mirror rather than a functional assistant. This half-measure suggests that OpenAI is still navigating the massive liability minefield of the financial sector. The moment an AI is empowered to execute transactions, it moves from being a software provider to a fiduciary entity, a transition that carries regulatory requirements OpenAI may not be ready to shoulder.

Furthermore, the reliance on Plaid creates a single point of failure that contradicts the decentralized ethos often touted in the tech world. If the connection between Plaid’s servers and OpenAI’s infrastructure hiccups, the user’s financial "brain" goes dark. We are watching the consolidation of financial oversight into a very small number of hands, where a handful of APIs dictate the visibility of our own wealth. For a company that started with the goal of democratizing AI, building these "walled gardens" of financial data feels like a pivot toward the very corporate gatekeeping that early AI proponents once criticized.

Ultimately, the long-term implication is a shift in how we perceive financial literacy. There is a risk that by outsourcing the cognitive labor of budgeting to a chatbot, users may become less aware of their own financial health, not more. If the AI handles the "why" and the "how," the human user becomes a passive recipient of instructions. We might be moving toward a future where we don't understand our money better; we just have a more articulate way of being told we’re broke.

Giving an AI access to your bank account is the ultimate test of the 'move fast and break things' era—let's just hope the only thing it breaks is your habit of ordering expensive artisanal toast, and not the actual global banking system.

Artūras Malašauskas is an AI Systems Integrator with 20+ years of production-grade web engineering experience. He has designed, shipped, and scaled enterprise Python/PHP systems for logistics, SaaS, and public-sector clients. For the past year, he has focused exclusively on AI integrations: deploying open-source LLMs, building generative media pipelines (image, audio, video), and engineering multi-agent workflows for real production environments. His standard: reproducibility, security, cost-efficient inference—no vaporware. He documents and evaluates emerging AI tooling, separating verified capabilities from marketing noise. Technical editor at: muza-ai.eu, ai-verslas.lt, ai-naujinos.lt Connect on LinkedIn

Comments