The Agentic Shift: Duck Creek’s Multi-Million Dollar Bet on Autonomous Insurance

Let’s be honest: the insurance industry hasn’t exactly been the poster child for "speed of light" innovation. For years, the sector has been bogged down by fragmented manual processes and legacy systems that make a simple claim feel like a marathon. But that narrative is shifting. Duck Creek Technologies has just thrown down a significant gauntlet, unveiling an insurance-native Agentic AI Platform designed to move beyond simple chatbots and into the realm of autonomous, goal-oriented "agents" that actually do the heavy lifting.

We're not just talking about another layer of generative AI that spits out summaries. According to FutureCIO, this platform is "purpose-built" to orchestrate and govern AI agents across the entire insurance lifecycle. It’s a bold move, especially when you consider that Boston Consulting Group expects AI to have an \$80 billion annual impact on the U.S. insurance market alone. Duck Creek clearly wants a piece of that pie, and they're doing it by embedding intelligence directly into the core workflows where decisions—and mistakes—usually happen.

Underwriting Without the Paper Trail

The first standout application is the Agentic Underwriting Workbench. If you’ve ever worked in underwriting, you know the "submission-to-quote" shuffle is where good deals go to die in a pile of PDFs. This new tool uses agents to intake, triage, and enrich submissions in real-time. As noted by Reinsurance News, the goal is to produce "decision-ready" submissions, letting human underwriters focus on the high-value risks rather than hunting down missing data fields.

What makes this work isn't just raw processing power; it’s what Duck Creek calls "neuro-symbolic reasoning." It’s a fancy term for a smart combination: it uses the creative, probabilistic nature of Generative AI but grounds it with the hard, deterministic rules of insurance policy logic. It’s basically giving the AI a set of guardrails so it doesn't hallucinate a new coverage limit that doesn't exist. This ensures every action is traceable and compliant—a non-negotiable in such a heavily regulated field.

Claims: From "First Notice" to Fast Resolution

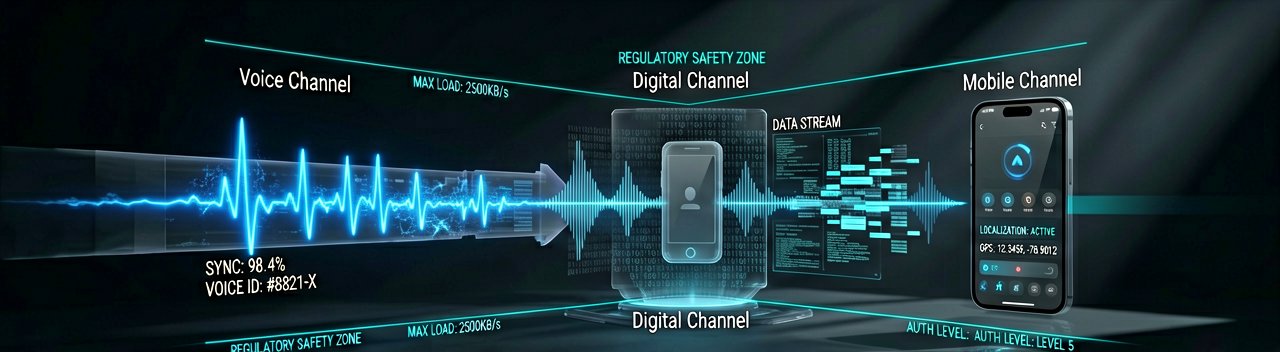

On the flip side of the house, the Agentic First Notice of Loss (FNOL) application is aimed squarely at the claims experience. Developed in collaboration with Google Cloud and powered by their Gemini models, this isn't your average automated phone tree. These agents can coordinate across digital, voice, and mobile channels to validate coverage and even sniff out early-stage fraud at the very moment a claim is filed.

By capturing higher-quality data right at the start, carriers can slash cycle times and lower loss adjustment expenses. But more importantly for the policyholder, it means getting an answer—or a check—faster. In a world where customer loyalty is increasingly tied to the ease of a claim, this kind of "intelligent" intake is becoming a survival trait rather than a luxury.

The Governance Layer: Trusting the "Agent"

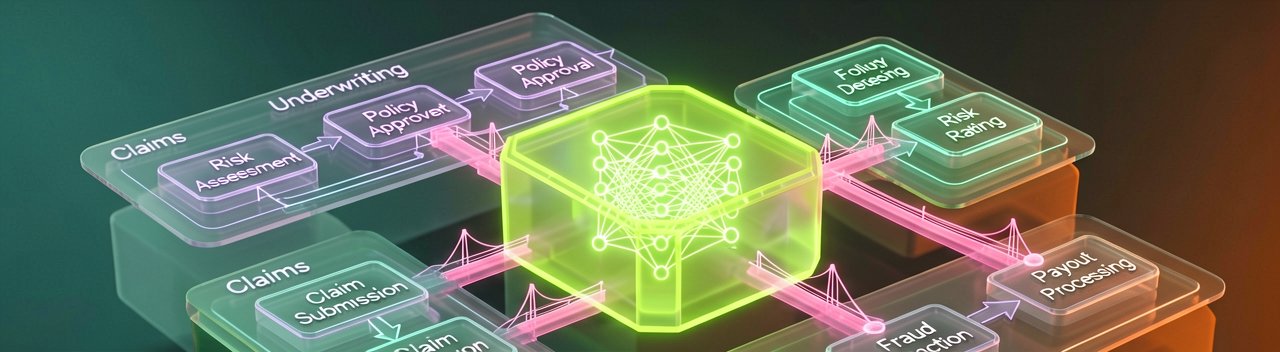

Of course, the big question with any autonomous system is: who’s watching the watchers? Duck Creek’s platform includes a dedicated "AI Assurance" layer. This provides the auditability and observability that risk-averse carriers crave. As reported by Yahoo Finance, the architecture includes a Model Context Repository (MCR) and an open "AI Gateway," allowing insurers to integrate their own models or partner-built agents into a governed framework.

Ultimately, Duck Creek isn't just selling a new tool; they're betting on a future where "agentic" becomes the standard. It’s an evolution from "AI as an assistant" to "AI as a workforce." If they can deliver on the promise of end-to-end orchestration without sacrificing compliance, the insurance back office might finally start moving as fast as the rest of the tech world.

The Real Pivot: While the headline centers on the "agentic" buzzword, the true story here is about Duck Creek attempting to solve the "last mile" problem of insurance digital transformation. For a decade, carriers have been told that moving to the cloud would solve their agility issues, yet many found themselves just as stuck—only now they were paying subscription fees for cloud-based silos. This platform represents a strategic shift from passive data storage to active logic execution, signaling a move where the core system isn't just a ledger, but an active participant in risk assessment.

What veteran industry watchers find most compelling is the departure from "Prompt Engineering" toward "Workflow Orchestration." Most early generative AI implementations in insurance failed because they were essentially islands; a claims adjuster might use a LLM to summarize a doctor’s note, but they still had to manually copy-paste that summary into three other legacy systems. Duck Creek’s agentic approach aims to kill the copy-paste culture by allowing these agents to cross system boundaries—interacting with policy, billing, and claims data simultaneously without a human babysitter.

The Shift from Chat to Action

There is a massive psychological hurdle in the c-suite when it comes to "Agentic AI." Historically, insurance software followed strict "if-then" logic—if the roof is 20 years old, then deny the windstorm coverage. Agentic AI, however, is probabilistic. It "thinks" in terms of likelihoods. To bridge this gap, Duck Creek’s integration with Google’s Gemini models isn't just about speed; it’s about a specific type of reasoning that can handle the messy, unstructured data found in legal depositions or medical records while adhering to the rigid constraints of a signed contract.

From a stakeholder perspective, this isn't just a win for the IT department. Chief Claims Officers are looking at this as a way to combat the "Great Resignation" in the adjuster space. The industry is facing a massive talent drain as seasoned adjusters retire, taking decades of institutional knowledge with them. By embedding that "expert logic" into agentic workflows, carriers aren't just automating tasks; they are effectively digitizing the intuition that used to take a human twenty years to develop.

Governance: The Elephant in the Underwriting Room

However, we can't ignore the regulatory tightrope. Insurance is arguably the most litigious and scrutinized industry in the world. If an AI agent autonomously denies a claim or raises a premium, the carrier must be able to explain *why* to a state regulator. This is why the "Neuro-symbolic" aspect of the platform is the most critical technical detail. It provides a digital paper trail—a "log of logic"—that turns the black box of AI into a glass box that an auditor can peer into.

Looking back, we’ve seen similar hype cycles with Blockchain and IoT in insurance, both of which struggled because they required the entire ecosystem to change at once. Duck Creek’s play is smarter because it’s backwards compatible. It doesn't require a carrier to throw away their existing data; it just puts an intelligent "agent" on top of it to start doing the work humans are too burnt out to manage. It’s a pragmatic evolution that acknowledges the industry's messy reality while pushing it toward a more autonomous future.

The Reality Check: Beneath the polished veneer of "agentic autonomy" lies a fundamental friction point: the insurance industry’s pathological obsession with certainty. Duck Creek is promising a world where AI agents navigate the gray areas of risk, yet the very foundation of insurance law is built on black-and-white contracts. There is a glaring contradiction in deploying "probabilistic" engines—systems that essentially make very educated guesses—within an industry that loses billions when a single word in a policy is misinterpreted.

We have to ask if carriers are truly ready to take their hands off the wheel. While the Agentic Underwriting Workbench sounds like a productivity miracle, it introduces a new kind of "model risk" that most actuarial departments aren't equipped to quantify. If an agent triages a submission incorrectly because of a subtle bias in its training data, the resulting "decision-ready" file is essentially a fast-tracked mistake. The speed of AI doesn’t just accelerate efficiency; it accelerates the rate at which systemic errors can propagate through a book of business.

The Integration Illusion

There is also the persistent myth of "seamless integration." Duck Creek’s open AI Gateway is a noble architectural goal, but it assumes that the messy, heterogeneous data of the average mid-market carrier will play nice with advanced Google Gemini models. In practice, most insurance data is trapped in "zombie systems"—decades-old databases that were never meant to talk to a modern API, let alone an autonomous agent. The risk here is that carriers spend millions on an agentic platform only to find their agents are "brilliant" but "blind," unable to access the very data they need to be effective.

Furthermore, the move toward Agentic FNOL (First Notice of Loss) could inadvertently alienate the very customers it seeks to serve. While a tech-savvy claimant might appreciate a 30-second automated validation, a person standing in a flooded basement or a wrecked car often wants a human, not a hyper-efficient "agent" that validates their coverage with clinical precision. There is a fine line between a frictionless experience and one that feels dismissive, and the industry has a spotty track record of knowing where that line is drawn.

Ultimately, the success of this platform won't be measured by the sophistication of its "neuro-symbolic reasoning," but by the courage of the compliance departments. If the "AI Assurance" layer is so restrictive that it flags every autonomous action for human review, then we haven't actually created an agentic workforce—we’ve just created a very expensive, very fast drafting tool. The industry is currently in a "trust, but verify" phase, but for Duck Creek’s vision to work, they will eventually have to drop the "verify" part, and that is a leap of faith many insurers may not be ready to take.

Projecting forward, we may see a tiered insurance market: "Premium" carriers who market their human-centric empathy, and "Algorithmic" carriers who compete solely on the speed and price dictated by their agents. Duck Creek has provided the engine for the latter, but the industry still hasn't decided if it's ready to let a machine write the rules of the road.

"Insurance has spent a century trying to turn humans into predictable machines; now that we finally have actual machines to do the work, we’re terrified they might act too much like humans."

Artūras Malašauskas is an AI Systems Integrator with 20+ years of production-grade web engineering experience. He has designed, shipped, and scaled enterprise Python/PHP systems for logistics, SaaS, and public-sector clients. For the past year, he has focused exclusively on AI integrations: deploying open-source LLMs, building generative media pipelines (image, audio, video), and engineering multi-agent workflows for real production environments. His standard: reproducibility, security, cost-efficient inference—no vaporware. He documents and evaluates emerging AI tooling, separating verified capabilities from marketing noise. Technical editor at: muza-ai.eu, ai-verslas.lt, ai-naujinos.lt Connect on LinkedIn

Comments