The $18 Million Moonshot: Is Rivian the Ultimate AI Sleeper Hit?

If you're hunting for the next great wealth generator, you've likely seen the headlines: $1 million today could balloon into a life-changing $18.7 million by 2032. It sounds like a fever dream from the 1990s dot-com boom, but in the world of artificial intelligence, these exponential trajectories are becoming the new baseline for speculative growth. The stock in question isn't a trillion-dollar titan like Nvidia—it’s Rivian Automotive (RIVN), a company increasingly being viewed as a "software-first" AI play disguised as an EV maker, according to analysis from The Motley Fool.

The math behind this staggering 1,770% projected return relies on a specific historical precedent: Tesla. If you had dropped $1 million into Tesla back in 2019, you’d be sitting on roughly $18.7 million today, as noted by Yahoo Finance . Rivian is currently standing at a similar crossroads. While the market has beaten the stock down—shares are down about 25% since the start of 2026—the underlying AI catalyst is just beginning to fire up. The "boring" days of just selling trucks are evolving into a high-margin ecosystem of autonomous software and intelligent fleet management.

The AI Assistant That's Outpacing Tesla

Rivian’s real secret sauce isn’t just its battery tech; it’s the intelligence inside the cabin. The company recently rolled out a new AI assistant that can control almost every vehicle function via voice—from climate settings to adjusting ride height. This is a feat that even Tesla’s Grok integration hasn't quite mastered yet, per reports from AOL. By building software-defined vehicles from the ground up, Rivian is positioning itself as a platform for AI applications, which carries the kind of recurring revenue and massive margins that hardware alone can't touch.

For investors with a high risk tolerance, the timing is critical. The massive growth catalyst for Rivian is expected to hit in the coming months as deliveries for its more affordable R2 SUV begin, as highlighted by MSN. This move into the mass market, combined with their proprietary AI robotics stack, could be the trigger that shifts the valuation from a struggling EV startup to an AI powerhouse. It’s a long-shot bet for sure, but for those looking to replicate the Tesla "millionaire-maker" era, the blueprint is remarkably similar.

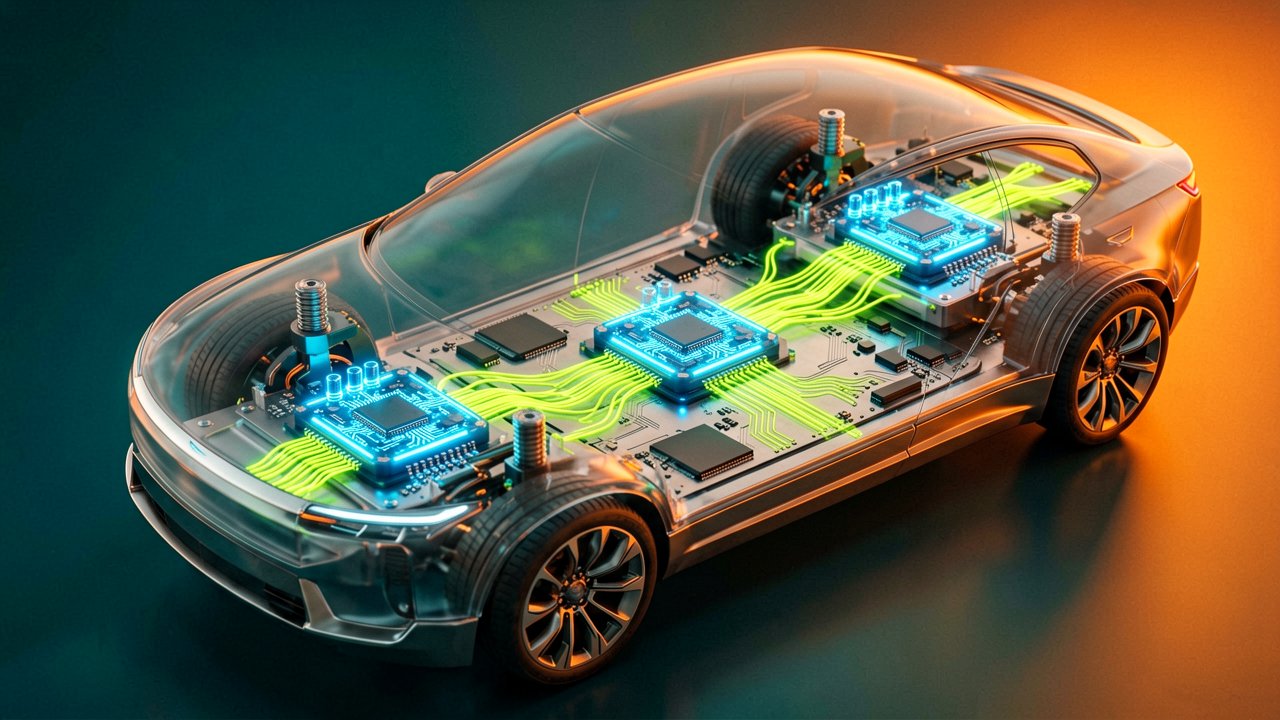

The Quiet Pivot: While the mainstream financial press is obsessed with quarterly delivery numbers and battery ranges, they are largely missing the structural transformation happening under Rivian’s hood. To understand the $18.7 million trajectory, you have to look past the R1S chassis and into the "zonal architecture" that defines their new platform. Most legacy automakers are still wrestling with a "spaghetti" mess of hundreds of independent electronic control units (ECUs) provided by third-party vendors. Rivian has consolidated this into just a few high-powered computers running their own proprietary operating system.

This isn't just a technical flex; it’s a massive economic moat. By controlling the "brain" of the car, Rivian can harvest data across every sensor in real-time, feeding a machine-learning loop that improves autonomous driving and energy efficiency faster than a traditional manufacturer ever could. As a seasoned tech reporter would tell you, the value here isn't the steel and rubber—it's the data. In the eyes of institutional bulls, Rivian is essentially a robotics company that happens to build things with four wheels, a distinction that justifies a tech-style valuation rather than a manufacturing one.

The Volkswagen Factor and the Software War

We also have to talk about the $5 billion elephant in the room: the Volkswagen joint venture. Critics initially saw the VW partnership as a mere lifeline for a cash-strapped startup, but insiders view it as a massive validation of Rivian’s AI stack. Volkswagen isn't just buying batteries; they are paying for access to Rivian’s software-defined vehicle architecture. This provides Rivian with a massive influx of capital without the dilution usually associated with equity raises, effectively de-risking the path to 2032 while scaling their software footprint across millions of non-Rivian vehicles.

However, the road to a 1,770% return is paved with execution risk. The company is currently burning through cash as it scales its Georgia manufacturing plant, and the "Tesla-like" ascent assumes they can reach positive gross margins by the end of this year. Stakeholders are watching the upcoming R2 launch with bated breaths; it is the make-or-break moment for the brand. If Rivian can successfully bridge the gap between "luxury niche" and "mass-market AI mobility," the 2032 projections might actually look conservative in hindsight. It’s a high-stakes poker game where the pot is the future of the American automotive industry.

The Reality Check: Before we start picking out upholstery for our hypothetical yachts, we need to strip away the "AI" buzzwords and look at the brutal physics of the balance sheet. The assumption that Rivian will follow the exact parabolic arc of Tesla is a seductive piece of survivorship bias. Tesla’s ascent happened in a vacuum of competition and a world of zero-percent interest rates. Today, Rivian is attempting to scale in a crowded arena where every legacy player from Hyundai to Ford is clawing for market share, often while subsidizing their EV losses with internal combustion profits—a luxury Rivian simply doesn't have.

There is also a fundamental contradiction in the "software-first" narrative. While we tout Rivian as a high-margin AI play, the company is still tethered to the physical world of supply chains, lithium costs, and labor unions. You can iterate software in a week, but building a multi-billion dollar factory in Georgia takes years and an astronomical amount of capital. If the R2 launch faces the same "production hell" that nearly killed Tesla in 2018, the runway might run out before the AI revenue has a chance to take off. Skeptics argue that the market is currently pricing Rivian as a car company because, well, it still mostly makes cars.

The Valuation Gap and the AI Mirage

Furthermore, we have to ask if the "AI assistant" and "zonal architecture" are truly unique enough to command a trillion-dollar valuation by 2032. Every major OEM is currently rebranding as a tech company; Mercedes-Benz is developing its own MB.OS, and Chinese giants like BYD and Xiaomi are moving at a speed that makes Silicon Valley look lethargic. Rivian’s moat is real, but it is shallow. To turn $1 million into $18 million, Rivian doesn't just need to be good; it needs to achieve a level of dominance that effectively renders the rest of the industry obsolete in the eyes of the consumer.

Projecting out to 2032 also ignores the "macro" wildcards. Trade wars, shifting subsidies, and the potential for a plateau in EV adoption could all derail this 1,770% moonshot. Investors aren't just betting on Rivian’s code; they are betting that the global economy will remain stable enough to support a luxury-to-mass-market transition for a decade. It’s a calculated gamble on a company that is currently a very expensive, very impressive underdog. Whether that underdog can become the alpha of the AI age remains a question that won't be answered by a spreadsheet, but by the grit of their manufacturing floor.

"Investing in an EV startup for its AI potential is a bit like buying a house for the smart thermostat: it’s a brilliant piece of technology, but you’ll feel pretty silly if the roof isn't finished by the time it starts raining."

Artūras Malašauskas is an AI Systems Integrator with 20+ years of production-grade web engineering experience. He has designed, shipped, and scaled enterprise Python/PHP systems for logistics, SaaS, and public-sector clients. For the past year, he has focused exclusively on AI integrations: deploying open-source LLMs, building generative media pipelines (image, audio, video), and engineering multi-agent workflows for real production environments. His standard: reproducibility, security, cost-efficient inference—no vaporware. He documents and evaluates emerging AI tooling, separating verified capabilities from marketing noise. Technical editor at: muza-ai.eu, ai-verslas.lt, ai-naujinos.lt Connect on LinkedIn

Comments